Understanding Your 1099-R

If you’ve received a 1099-R this tax season, you may be wondering what it is, why it arrived, and what you need to do with it. Let’s walk through the basics and answer some of the most common questions we hear from ministers and church staff.

What Is a 1099-R?

Form 1099-R is an IRS tax form used to report distributions taken from a retirement account. These forms are issued by the end of January each year, and both you and the IRS receive a copy.

You will receive a 1099-R from any institution from which you took a distribution during the year. If you took more than one type of distribution, you may even receive multiple 1099-Rs from the same institution.

What Types of Distributions Are Reported?

Several kinds of retirement account distributions are reported on a 1099-R, including:

- Withdrawals

- Required Minimum Distributions (RMDs)

- Death distributions

- Housing allowance distributions

Even distributions not received directly by the account holder are still reportable. These include charitable gifts paid directly from your retirement account, as well as conversions and rollovers.

The only transactions not reported on a 1099-R are direct transfers between “like” retirement accounts, such as:

- Traditional IRA to Traditional IRA

- Roth IRA to Roth IRA

- 403(b) to 403(b)

Because these transfers are not considered distributions, they do not appear on the form.

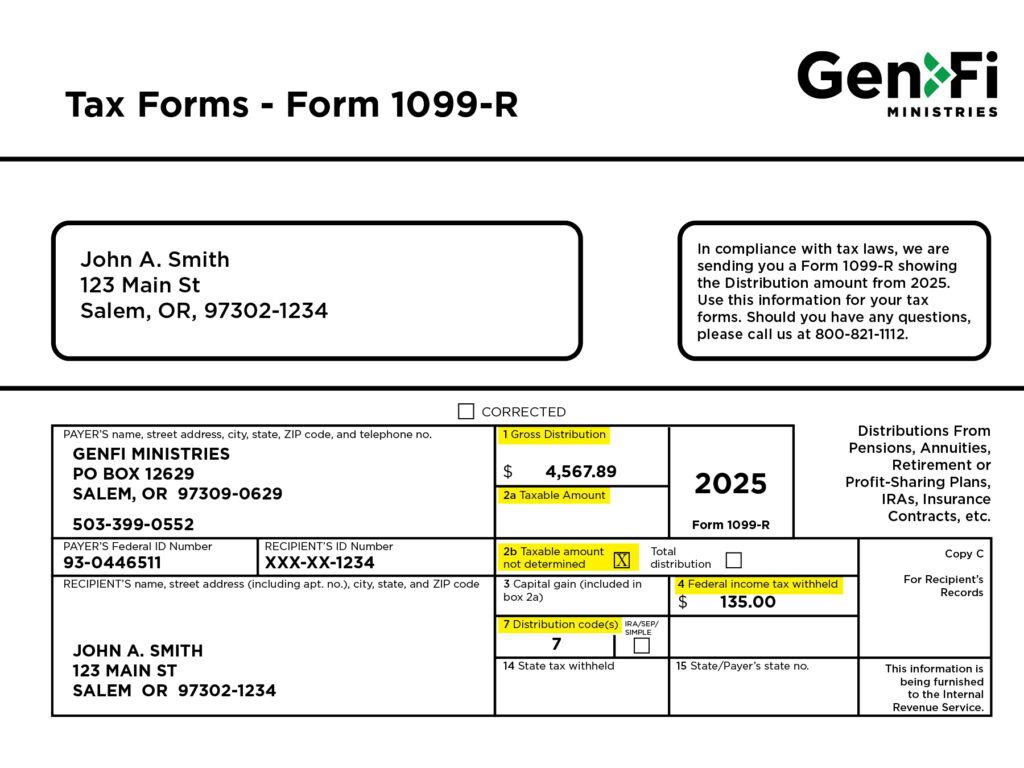

How to Read the Key Boxes on Your 1099-R

Understanding the boxes on your 1099-R can help clarify what was reported and why.

Box 1: Gross Distribution

This box shows the total amount of the distribution taken during the year.

Box 2a: Taxable Amount

This box may show a taxable amount determined by the institution based on the distribution code. Often, it is left blank, which means the taxpayer is responsible for determining whether the distribution is taxable.

Box 2b: Taxable Amount Not Determined

If Box 2a is blank, Box 2b is typically checked. This indicates that determining the taxable portion of the distribution is left to the taxpayer.

Box 3: Capital Gain

This box is generally blank and applies only to certain taxable death benefit lump-sum distributions.

Box 4: Federal Income Tax Withheld

This shows how much federal income tax was withheld from the distribution and sent directly to the IRS as a prepayment of taxes owed. If you do not owe tax, or if too much was withheld, you may receive this amount back as part of your refund.

Box 7: Distribution Code

Box 7 identifies the type of distribution using an IRS code. The definitions can be found on the back or second page of your 1099-R. Some of the most common codes include:

- 7 – Normal distribution (age 59½ or older)

- 4 – Death distribution from an inherited or beneficiary retirement account

- 1 – Early distribution (under age 59½ and may be subject to a 10% penalty)

- G – Rollover to another qualified plan or IRA, either direct or completed within 60 days

- Y7 – Direct transfer to a charity by an individual over age 70½

- (Code Y4 is used for charitable transfers from inherited retirement accounts)

Frequently Asked Questions

Why Is My Housing Allowance Distribution Showing on the 1099-R?

Housing allowance distributions are generally not taxable, but they are still reportable. Submitting a Housing Allowance form to an institution allows you to waive federal withholding on the distribution, but it does not remove the requirement to report it on a 1099-R.

It is the account holder’s responsibility to ensure they qualify to claim the specified amount as a housing allowance and to report the correct taxable amount on their tax return.

Why Is My Qualified Charitable Distribution Showing on the 1099-R?

Qualified Charitable Distributions (QCDs) are generally not taxable, but they must still be reported as distributions. Distribution codes Y7 or Y4 are used to identify these amounts as charitable gifts.

We’re Here to Help

If you have questions about your 1099-R or any of your retirement distributions, our team is happy to help.

Email: retirement@cepnet.com

Phone: 800-821-1112

Understanding your tax forms can feel overwhelming, but a little clarity goes a long way. We’re here to walk alongside you and help you steward your retirement with confidence.

This article was posted by Ryan Kropf on behalf of the author, Bethany Tranby, RICP®.